The best way to distinguish between liabilities and expenses is by analyzing cash flow. Expenses are costs that have been incurred to generate revenue, but may or may reporting partnership tax basis not have been paid. For example, XYZ Company purchased a computer on January 1, 2016, paying $30,000 upfront in cash and with a $75,000 note due on January 1, 2019.

Interest expense journal entry

If interest expense is the cost of borrowing money, interest income is the interest percentage you would receive if your business is the party lending the cash. This means that at the end of the fiscal year the company has to pay $250 to cover their interest expense. If you want to calculate the monthly charge, just divide the interest expense by 12. In most cases, you won’t have to calculate the interest due yourself – financial institutions will send you a breakdown of the cash owed. And if you’re using an online accounting system, the software can calculate this for you. Recording interest allocates interest expenses to the appropriate accounts in your books.

- The interest rate was 10% per annum, and they needed to pay the interest expense 20 days after each month ended.

- For example, a company has borrowed $1,000,000 from ABC bank at the interest rate of 10% p.a.

- Interest payable is typically combined with other current liabilities on the balance sheet, but it may also be presented as a separate line item.

How To Calculate?

When a company pays its interest expense, the journal entry will require a debit to the interest payable account and a credit to the cash account. Interest payable is a current liability on the balance sheet that reflects the amount of interest a company owes to its creditors. It is usually accrued each month’s end and is an important liability for the company. You typically need to adjust entries when you see a difference between cash flow and the accrual basis of accounting. For example, you might pay for expenses in advance and adjust the prepaid expense account to reflect the portion used up during the period.

How often should I make journal entries in my small business?

This ensures that the company’s financial statements are accurate and up to date. It also enables the company to track the interest payments and determine if any adjustments need to be made to the amount due. Interest payable, on the other hand, is a current liability for the part of the loan that is currently due but not yet paid.

And the rest of the amount (i.e., $6000) wouldn’t take place on the balance sheet. This includes considering the notes payable, which is the amount that an individual or entity plans to borrow. This allows the businesses to be more accurate while calculating the interest expense for the period. Interest payable on balance sheet tells firms and keeps them alarmed about the financial obligations they have to fulfill. If any interest incurs after the date at which the interest payable is recorded on the balance sheet, that interest wouldn’t be considered. The interest can be compounded, meaning that interest is added to the principal amount of the loan and then the interest is charged on the new balance.

The creditors charge interest to the company base on the interest rate and accounting period. The customer record interest expense base on this period as well, it will not be related to the payment. When the company borrows money from a bank or other creditors, it will record it as debt on the financial statement. The company is required to pay back this debt plus an extra cost which is the interest expense. Except if the interest expense is paid in advance, the organization will always have to record interest payable in its balance sheets statements to report the interest paid to the lender.

Accrued interest is included in a separate accrued interest liability account on the balance sheet. Payable interest is an obligation regardless of whether the debt is short-term or long-term. Companies must pay interest on all outstanding debt, and this must be reflected accurately on the balance sheet. In general, it is reporting in the current liabilities rather than non-current.

To meet this need, it issues a 6 month 15% note payable to a lender on November 1, 2020 and collects $500,000 cash from him on the same day. The Maria will repay the principal amount of debt plus interest @ 15% on April 30, 2021, at which date the note payable will come due. The company can make the interest expense journal entry by debiting the interest expense account and crediting the interest payable account. The yield is 10%, the bond matures on January 1, 2022, and interest is paid on January 1 of each year. So if the question asks how much cash was paid for interest in a particular period, then we know the question will need to provide accrual basis information. For example, the question might tell us that the beginning interest payable balance was $15,000 and the ending interest payable balance was $5,000.

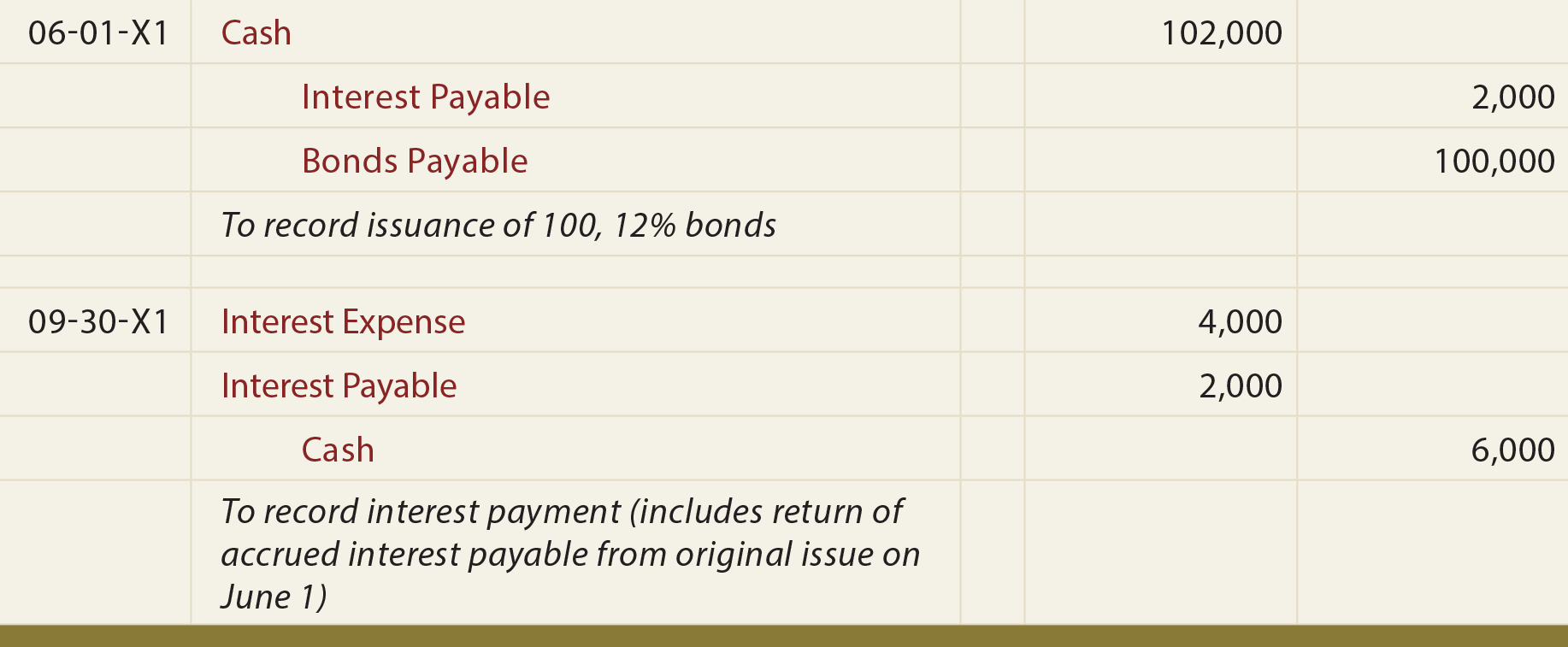

Sometimes corporations prepare bonds on one date but delay their issue until a later date. Any investors who purchase the bonds at par are required to pay the issuer accrued interest for the time lapsed. The company assumes the risk until its issue, not the investor, so that portion of the risk premium is priced into the instrument. Accrued interest is usually counted as a current asset, for a lender, or a current liability, for a borrower, since it is expected to be received or paid within one year. We take monthly bookkeeping off your plate and deliver you your financial statements by the 15th or 20th of each month.